-

ABOUT

-

-

-

-

CONTACT

Turbulence on the supply side is brewing again—what lies ahead for aluminum prices?

At the beginning of this month, LME aluminum outperformed other nonferrous metals, as concerns about overseas supply intensified following Hydro’s decision to further scale up production cuts and reports that the LME may ban trading in Russian metals, driving LME aluminum prices up by more than 8% at one point. On Monday this week, SHFE aluminum followed suit, rising 1.56% on the back of these developments. However, as the holiday-related positive factors were largely priced in and domestic COVID-19 cases began to resurge, SHFE aluminum fell for two consecutive days, giving up its earlier gains. Meanwhile, LME aluminum posted modest cumulative gains this week, extending its winning streak to two straight weeks.

Europe’s energy shortage remains difficult to alleviate, and European aluminum producers still face the risk of production cuts.

Natural gas accounts for more than 20% of Europe’s electricity generation. As of October 10, the IPE UK natural gas futures settlement price closed at 298 pence per therm, up 86% from the start of the year. Persistently high power costs have prompted overseas aluminum producers to further expand production cuts; by mid-September, European primary aluminum smelters had collectively reduced output by nearly 1.5 million tonnes, representing 15% of the region’s total installed capacity.

On September 26, natural gas leaks occurred on two undersea pipelines that supply Russian gas to Europe, with no prospect of resuming operations in the near term. As the heating season approaches, reduced gas supplies combined with the ongoing instability in the Russia-Ukraine situation are keeping electricity costs elevated, leaving European aluminum producers still at risk of production cuts.

On September 30, market sources reported that the LME is considering removing aluminum produced by Rusal from its delivery roster. Russia is a major aluminum producer, with Rusal boasting an annual capacity of roughly 4.5 million tonnes—making it the world’s largest aluminum producer outside China and accounting for 6% of global supply, or 13% of non-Chinese primary aluminum capacity. From January to August 2022, China’s cumulative imports of primary aluminum totaled 297,600 tonnes, with Rusal accounting for 77% of the country’s total imports. Should this metals ban be formally implemented, there is a possibility that some of Rusal’s output could still find its way into the Chinese market. Notably, China’s reliance on imported primary aluminum is relatively low, representing only about 3% of total supply; therefore, the focus should remain on domestic production.

Figure 1: List of Overseas Electrolytic Aluminum Production Cuts in 2021–2022. Data sources: SMM, Fueneng Futures.

The domestic oversupply situation in the electrolytic aluminum market has eased somewhat.

From January to September 2022, cumulative electrolytic aluminum output reached 29.8895 million tonnes, up 2.76% year on year. This year, the relaxation of China’s “dual-control” policy has led to a steady release of electrolytic aluminum capacity, initially putting significant pressure on the supply side. However, following Sichuan’s production cuts in August, Yunnan further expanded its output reductions in September, with most Yunnan-based smelters now cutting production by 20%, totaling 1.3 million tonnes—and it is unlikely that these cuts will be reversed during the dry season ahead. As a result, China’s operating electrolytic aluminum capacity fell rapidly in September to 40.227 million tonnes, substantially easing supply pressures. Consequently, the full-year forecast for electrolytic aluminum output has been revised downward to 40 million tonnes, representing a year-on-year increase of 2.64%.

Figure 2: China’s Operative Electrolytic Aluminum Capacity (in 10,000 tonnes). Data sources: Tonghuashun, Funeng Futures.

Affected by the warehouse incident at the end of May, hidden inventories of primary aluminum have increased, while overall social inventories have remained low. Since August, production cuts in Sichuan and Yunnan provinces due to power shortages have led to a moderate reduction in primary-aluminum supply, resulting in slower-than-expected inventory build-up. As of October 10, domestic social inventories of primary aluminum stood at 672,000 tonnes, down 191,000 tonnes from the same period last year. It is expected that by the end of October, domestic primary-aluminum inventories will be around 720,000 tonnes.

Figure 3: China’s Social Inventory of Electrolytic Aluminum (in 10,000 tonnes). Data sources: SMM, Funeng Futures.

Electricity prices still have room to rise, and electrolytic aluminum costs remain relatively firm.

In September, the average smelting cost of electrolytic aluminum was RMB 17,800 per tonne, with electricity accounting for the largest share at 34.36% of total costs, followed by alumina at 31.66%, and pre-baked anodes at 19.57%.

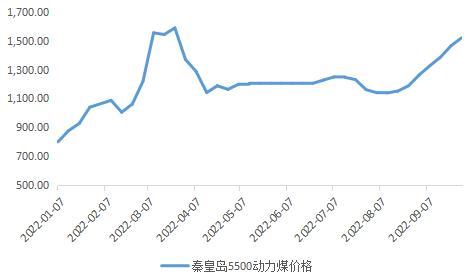

In the power sector, market coal supplies remain tight, driving up electricity generation costs. Strong thermal coal prices, coupled with constrained hydropower output in Yunnan, suggest that electricity tariffs are likely to continue rising.

Figure 4: Qinhuangdao 5,500 kcal/kg thermal coal price (RMB/ton). Data sources: Tonghuashun, Funeng Futures.

In the alumina sector, China’s alumina output from January to August 2022 reached 54.443 million tonnes, up 4.2% year on year. This year, newly commissioned alumina capacity is expected to total 13.2 million tonnes; however, due to the scarcity of domestic bauxite resources and increasing difficulties in procuring spot overseas bauxite, bauxite supply remains tight, leading some producers to cut output because of bauxite shortages. At the same time, electricity and bauxite prices have continued to rise, and cost pressures have prompted reductions in alumina capacity of about 2.9 million tonnes, thereby easing expectations of a severe oversupply. Overall, the pattern of oversupply in the alumina market is unlikely to change, and alumina prices are expected to trend lower in a volatile manner in October.

Figure 5: Alumina Price (RMB/ton) and Alumina Production (10,000 tons). Data sources: Tonghuashun, Funeng Futures.

Overall, although alumina prices are on a downward trend, the continued replenishment of power plants with high-priced coal is likely to push electricity prices higher. Meanwhile, the rising costs of petroleum coke and coal tar pitch have increased the production cost of pre-baked anodes, providing stronger price support and helping to maintain relatively firm electrolytic aluminum costs.

Figure 6: Electrolytic Aluminum Costs (RMB/ton). Data sources: Tonghuashun, Funeng Futures.

Downstream aluminum consumption continued to show marginal improvement in October.

With the easing of power restrictions, new orders in China’s downstream aluminum processing sector improved in September, driving the composite PMI for the sector up by 12.4 percentage points month-on-month to 57.9. Based on current order intake and production scheduling, downstream aluminum consumption is expected to continue showing marginal improvement in October, though it will still fall short of levels seen in the same period in previous years.

The real estate sector has been continuously rolling out favorable policies to stimulate housing demand. From January to August 2022, the year-on-year cumulative growth rates for completed and newly started residential floor space nationwide were –21.1% and –37.2%, respectively. On the completion front, driven by local governments’ mandates to ensure project delivery, conditions have gradually improved, showing a modest rebound compared with July. On the sales front, policy measures such as lowering the down-payment ratio and reducing first-home public housing fund loan rates by 15 basis points signal a policy shift. Going forward, the real estate market is expected to continue its recovery; however, it will still take a considerable amount of time before consumer spending genuinely picks up. Overall, real estate is forecast to weigh on aluminum consumption growth by around –2.3% for the full year.

From January to August, cumulative automobile production reached 17.35 million units, up 6.4% year on year, with the bulk of the increase attributable to new-energy vehicles. During the same period, NEV production totaled 4.074 million units, a year-on-year surge of 110.1%. Following the second quarter, improved pandemic conditions and the introduction of a series of policies to stimulate auto consumption have boosted vehicle sales. It is estimated that in 2022, NEVs will account for 5.18% of total aluminum consumption in the automotive sector, representing a month-on-month increase of 2.16 percentage points.

Domestic new photovoltaic installations continue to gain momentum, with cumulative additions reaching 44.47 GW from January to August, up 101.68% year on year. As PV prices and costs continue to decline in the future, demand for PV installations is expected to keep expanding, driving the share of aluminum consumption in the PV sector to 4.9% in 2022, a month-on-month increase of 0.2 percentage points.

From January to August 2022, cumulative exports of unwrought aluminum and aluminum products totaled approximately 4.7 million tonnes, up 31.5% year on year. With overseas aluminum smelters and aluminum processing firms operating at reduced capacity, domestic aluminum product exports are expected to remain supported; however, declining export margins and the global economic downturn are likely to further moderate the growth rate of aluminum exports.

Overall, demand in key aluminum-consuming sectors such as real estate remains weak. Although aluminum consumption in the new-energy-vehicle and photovoltaic industries continues to rise, the boost to overall demand is limited. Coupled with weakening overseas demand, aluminum-export growth has slowed, suggesting that demand is unlikely to improve significantly in the near term.

Summary

Overall, on the macro front, the IMF’s downward revision of its global growth forecast, stronger-than-expected nonfarm payrolls data, and hawkish comments from Federal Reserve officials have reinforced expectations of further rate hikes, driving the U.S. dollar higher and putting downward pressure on aluminum prices. On the fundamentals front, global primary aluminum supply is expected to continue contracting, with Europe’s energy shortages proving difficult to alleviate and aluminum producers still facing the risk of production cuts; domestically, Yunnan Province is likely to implement additional output reductions. On the demand side, downstream aluminum consumption has shown some signs of recovery, but overall remains below typical peak-season levels. At present, the directional bias remains unclear: strong cost support for primary aluminum caps downside potential, while any upside will depend on whether domestic consumption continues to improve. We expect aluminum prices to trade in a range of RMB 17,800–19,000 per tonne. (Futures Daily)

Previous page:

Henan Mingmei Magnesium Technology Co., Ltd.

Phone:+86-392-3658888 / 3659999

Email:hnmingmei@163.com

Address: Hebi National Economic and Technological Development Zone, Henan Province

Mobile

Copyright © Henan Mingmei Magnesium Technology Co., Ltd.